Variance

| Tags |

|---|

Variances

Variances are defined as follows:

(you can see why these are equivalent below)

Variances are not linear:

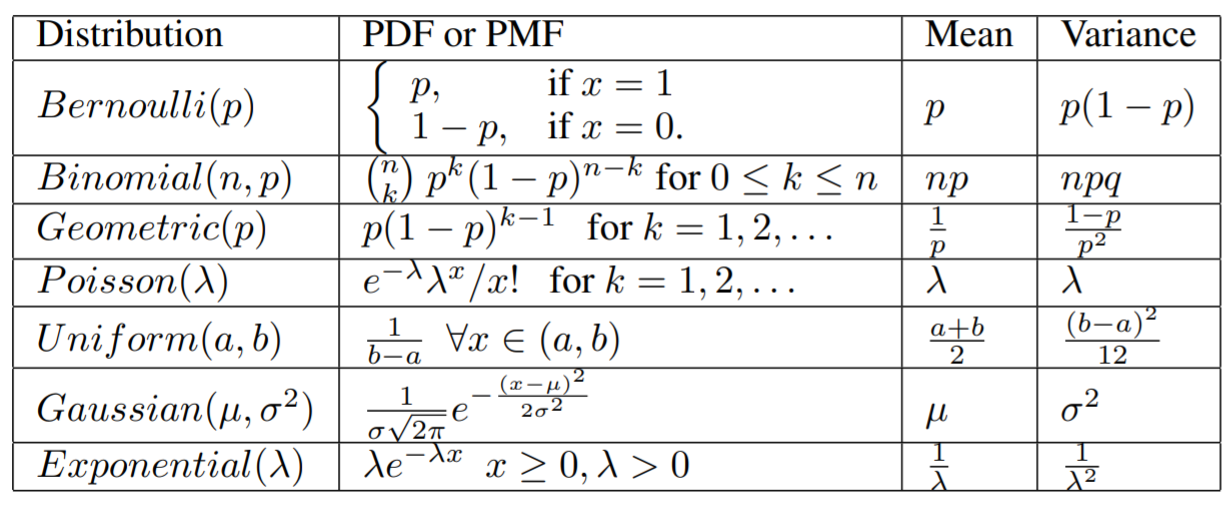

Stats of common random variables

| Tags |

|---|

Variances are defined as follows:

(you can see why these are equivalent below)

Variances are not linear: